With the rising number of high-profile incidents involving asset misappropriation fraud, the challenges faced by federal fraud investigators have never been more acute.

From public officials siphoning off funds to complex multinational fraud schemes, the scenario is intricate and demands attention.

With the task of scrutinizing immense volumes of physical and electronic financial records to identify fraud, investigators need innovative solutions. These solutions must not only simplify the processes but also equip them with analytics that provide deeper insights and evidence.

In this article, we take you through all the intricacies of asset misappropriation fraud and how you can deal with these schemes for the best possible outcome.

What is Asset Misappropriation Fraud?

Asset misappropriation fraud refers to the unauthorized use, theft, or embezzlement of an organization’s resources. It involves exploiting vulnerabilities within a company’s financial system to divert funds, steal assets, or manipulate financial records.

There are several types of asset misappropriation fraud, including:

- Cash theft at the cash register or petty cash drawer, where an employee may skim money before it’s recorded.

- Inventory Fraud includes stealing physical goods or manipulating inventory records.

- Illegal copying or stealing of a company’s proprietary information to buy assets.

- Manipulating the payment system to make unauthorized payments to oneself or others.

Common Techniques and Schemes Used in Asset Misappropriation

Each of the techniques discussed below represents a different facet of asset misappropriation fraud, requiring tailored prevention and detection strategies.

Proper understanding and continuous adaptation to emerging threats are essential to protect an organization from the following risks.

Embezzlement

This fraud scheme is often considered an inside job as it is typically carried out by employees who have access to the company’s finances. These individuals exploit their position and knowledge of the internal control systems to divert funds for personal use.

The steps they might take can include forging signatures, manipulating expense reports, creating phantom employees on the payroll, or using company credit cards for personal purchases.

For instance, a court in Washington, D.C. recently charged the founder and former CEO of a sustainable fuel company with embezzling at least $5.9 million from the company. As per the court documents, the person allegedly defrauded the company he founded by transferring company funds fraudulently to his personal bank account. The culprit allegedly attempted to conceal his embezzlement by emailing altered bank statements and other falsified financial records to the board members and the company accountant.

How can it be prevented?

Detection can be difficult due to the perpetrator’s intimate understanding of the company’s financial operations, making regular audits and strong internal controls essential for prevention.

Fake Vendors and Shell Companies

Creating fake vendors or shell companies is a more complex form of fraud that often involves collusion between employees and external parties.

Individuals in positions of authority create or use existing shell companies, then generate fake invoices for nonexistent goods or services. By approving these fraudulent transactions, they can divert company funds to these fake vendors. The funds received by the shell companies are then transferred to personal accounts.

For example, in a recent money laundering case, The former National Treasurer of Venezuela and her husband accepted over $136 million in bribes from a Venezuelan billionaire businessman who owned the Globovision news network. The fraud involved bulk cash hidden in cardboard boxes and offshore shell companies. As per the court documents, the bribes were used to purchase bonds from the Venezuela National Treasury at a favorable exchange rate, resulting in hundreds of millions of dollars of profit.

This type of scheme may involve multiple layers to make detection more challenging, including using genuine company names with slight alterations, falsifying supporting documents, and creating bogus physical addresses.

How can it be prevented?

Implementing rigorous vendor vetting processes and robust verification procedures for invoices and payments can help prevent this type of fraud.

Check and Payment Tampering

According to the Payments Fraud and Control Survey, checks were one of the most impacted payment methods by fraud activity (63%). This kind of tampering involves altering, forging, or manipulating checks and electronic payments to divert funds to unauthorized recipients.

Check and payment tampering techniques might include changing payee names, altering check amounts, or intercepting and altering electronic payment instructions. Employees responsible for payment processing are often the perpetrators, exploiting their position to bypass controls.

Let’s look into a real-life check fraud scheme executed by Scott Capps, a former employee of Vanguard, an investment management company, who defrauded both the company and the State.

Dormant accounts with abandoned funds that ideally should have gone to the State were accessible to Capps. Rather than submitting it to the state, he cleverly stole the passwords of his subordinates and used them to access the system, issuing checks on these dormant accounts to a co-conspirator and stealing over $2.1 million.

This kind of fraud activity highlights the need for efficient management of funds and the detection of suspicious transactions within companies.

Must explore: How can technology help in investigating transaction fraud?

How can it be prevented?

Employing secure payment methods, segregating duties, and regular reconciliation of accounts can mitigate these risks. Tools like ScanWriter’s check reader automatically read, capture, and organize data from all checks to custom Excel sheets, helping your business identify irregular transactions early on.

Skimming and Cash Larceny

Both of these involve the theft of cash, but at different stages of the transaction process.

Skimming occurs when an employee takes cash before it’s recorded in accounting records, such as stealing part of the cash sales before depositing the rest. Cash larceny is stealing cash after it has been recorded; for instance, taking money from the cash register after the sales have been logged.

How can it be prevented?

Both methods require the perpetrator to manipulate records to cover up the theft, making reconciliation and regular audits vital for detection.

Inventory Theft and Fraud

This type of fraud scheme refers to the physical theft of inventory and manipulating records to cover up the theft or inflate the value of inventory.

This might include falsifying receiving reports, altering shipping documents, or tampering with physical counts. The impact extends beyond the loss of physical goods, potentially affecting financial statements, tax liabilities, and investor confidence.

For example, in an alleged inventory fraud case, former executives and employees of Outcome, a privately held company based in Chicago, engaged in a massive five-year scheme to defraud multiple clients by selling advertising inventory they did not possess.

How can it be prevented?

Implementing stringent inventory control measures, employing surveillance systems, and conducting unannounced inventory counts can help uncover and prevent these schemes.

Phone Expenses and Reimbursement Schemes

These fraudulent schemes involve employees submitting fraudulent expense reports or inflating legitimate expenses to receive undue reimbursements.

Techniques might include submitting receipts for personal expenses as business expenses, claiming expenses for canceled trips, or inflating mileage and meal expenses.

This fraud capitalizes on weak expense approval processes and a lack of verification.

In 2022, the settlements under the False Claims Act exceeded $2.2 billion for the fiscal year. In a recent case, a vascular surgeon from Bay City, Michigan, was sentenced to 80 months in prison and a $19.5 million penalty for a multimillion-dollar fraud scheme by submitting claims for the placement of vascular stents and for thrombectomies that he did not perform.

How can it be prevented?

Establishing clear expense policies, requiring detailed documentation, and utilizing expense management software with built-in controls can be effective in preventing these schemes.

Also Read: Top 10 Most Notorious Asset Misappropriation Fraud Cases In US History

Detection and Investigation For Asset Misappropriation Fraud

Detecting and investigating asset misappropriation fraud requires a multi-faceted approach that combines technology, expertise, and collaboration.

Here’s a deeper look at the different aspects involved:

Data Analytics and Forensic Accounting Techniques

Modern technology enables the use of data analytics, statistical modeling, and forensic accounting to uncover discrepancies and patterns that may indicate fraud. Automated monitoring, pattern recognition, predictive analysis, and visualization tools help in spotting potential red flags.

Meanwhile, forensic accounting provides detailed examination, evidence gathering, litigation support, and collaboration with law enforcement. Together, they form a comprehensive and efficient methodology to combat fraud, ensuring speed, accuracy, and adaptability to emerging threats.

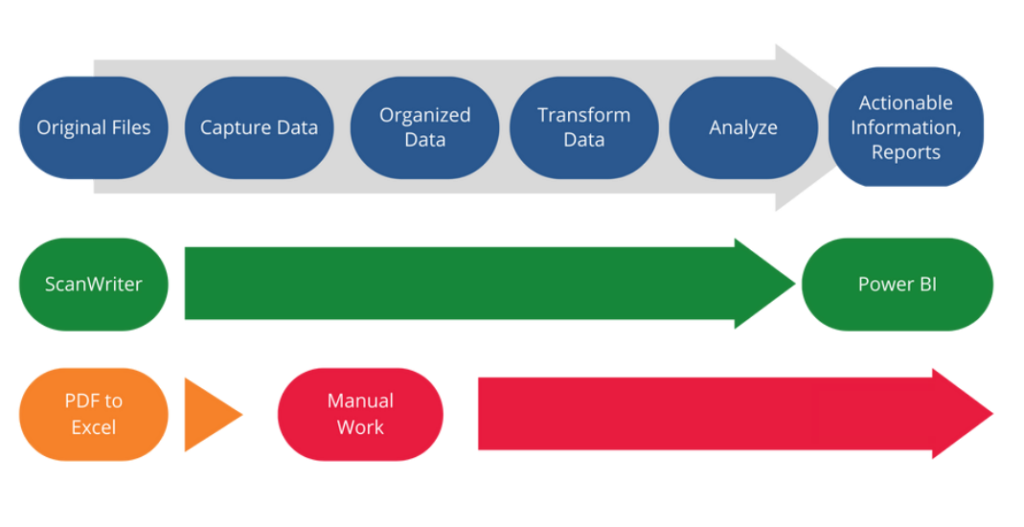

Tools like ScanWriter use advanced OCR technology for automated data capture at a very high speed. It can read 40000+ formats, collecting data from various sources like bank statements, invoices, and receipts. This data can be used to create visualizations to fast-track the money trail investigation.

Following the Money Trail

Tracing the flow of illicit funds and uncovering hidden assets is central to asset misappropriation investigations. Here’s how it’s done:

Tracing Illicit Funds and Hidden Assets

Investigators employ advanced tracing techniques to follow the movement of stolen funds through various accounts, shell companies, or offshore entities. This includes:

- Analyzing bank statements, wire transfers, and other financial records to pinpoint suspicious activities.

- Identifying real estate, investments, or other tangible assets purchased with illicit funds.

- If applicable, tracking transactions involving cryptocurrencies, which are often used to hide assets.

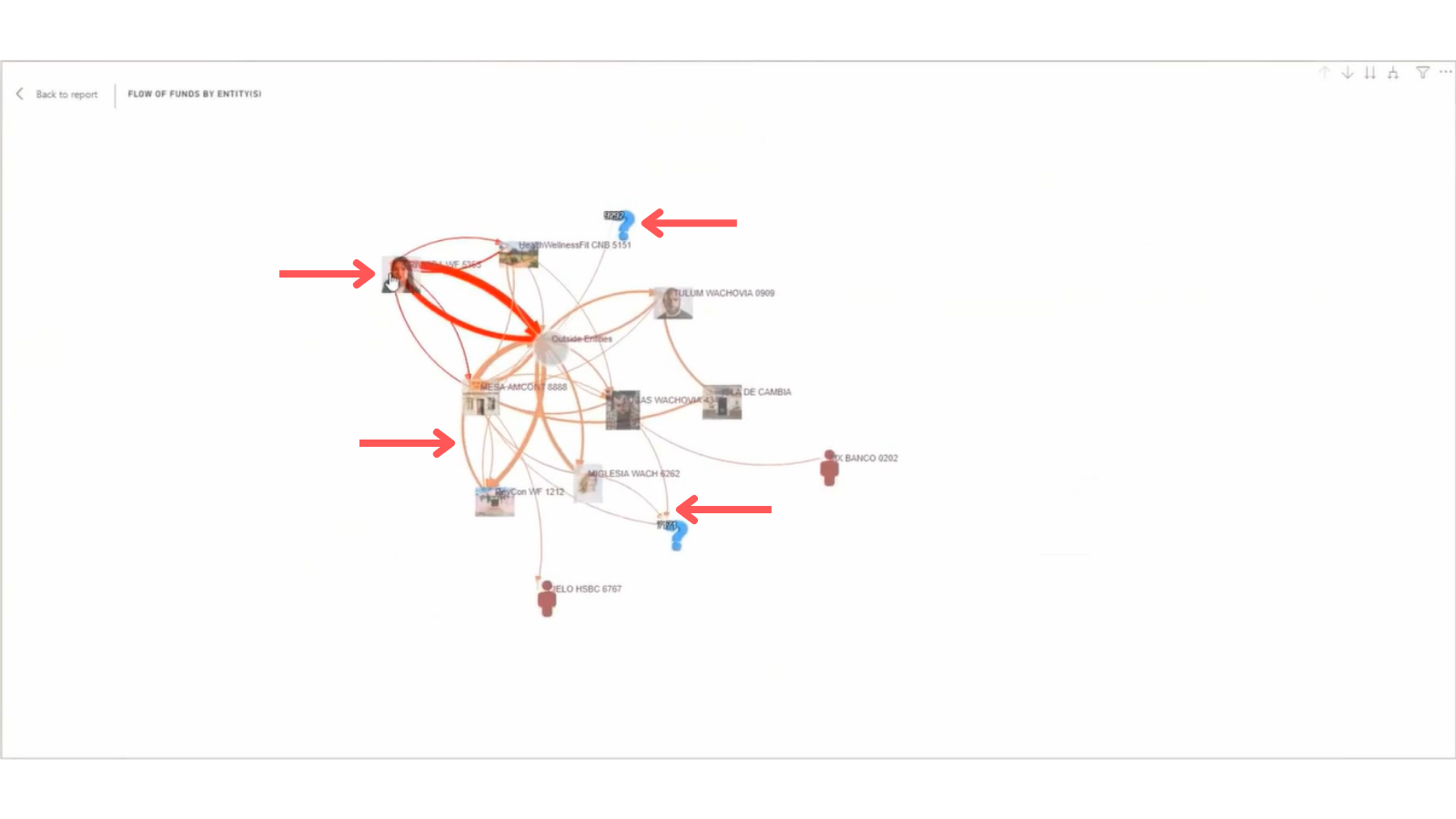

- Employing software like ScanWriter that can sift through large volumes of data, assisting investigators in connecting the dots between complex financial transactions. ScanWriter automatically populates the ‘Flow of Funds’ visualization and allows investigators to follow the money trail between different accounts by applying various filters like entities, transaction amounts, dates, etc.

ScanWriter – Asset Tracing

International Aspects of Asset Misappropriation Investigations

In an increasingly globalized world, fraudsters may use international channels to hide stolen assets. This adds complexity to investigations and requires:

- Compliance with different jurisdictions and coordination with international agencies.

- Working closely with law enforcement agencies in other countries to exchange information and support the investigation.

Cooperation with Other Law Enforcement Agencies

The complexity of asset misappropriation fraud often necessitates collaboration between various law enforcement agencies, regulatory bodies, and even private sector entities. Sharing intelligence, joint operations, and coordinated legal actions are essential components of this collaborative effort.

Building a Strong Case for Prosecution

Successfully prosecuting asset misappropriation fraud requires more than just merely identifying the perpetrators. Here’s how that’s achieved:

Gathering Sufficient Evidence

Collecting substantial evidence that can withstand legal scrutiny involves meticulous documentation, witness interviews, forensic analysis, and more. Every piece of evidence must be relevant, credible, and admissible in court.

The Role of Digital Evidence in Modern Fraud Investigations

In the digital age, emails, digital transactions, computer logs, and other electronic evidence play a crucial role. Proper collection, preservation, and analysis of digital evidence are vital, requiring specialized tools and expertise.

Working with Prosecutors and Legal Challenges

Building a prosecutable case requires close collaboration with prosecutors, understanding legal requirements, and overcoming challenges such as legal loopholes, jurisdictional issues, and more. The strategic partnership between investigators, forensic experts, and legal professionals ensures a cohesive and compelling legal case.

Real-Life Case Studies

Now that we have discussed various aspects of asset fraud schemes, let’s take a look at two real-life asset misappropriation case studies and how they were solved.

How Technology Helped Win an Embezzlement Case

A recent embezzlement case involving the misappropriation of public funds by a suburban city comptroller showcased the critical role of technology in fraud investigations.

The investigators had over 4,500 transactions and 993 pages of bank statements to analyze. Using ScanWriter’s data capture and analytics tool, they were able to process these files in just four hours, compared to the 74 hours manual processing would have taken.

The software not only streamlined the conversion of various documents into an organized Excel spreadsheet, but its integration with Power BI provided dynamic visualizations of the funds’ flow.

Various departments were able to collaborate in real-time through ScanWriter’s platform, ensuring effective communication. Data entry time was cut by 90% with 100% accuracy and financial models could be visualized – all of which contributed to presenting compelling evidence and, in turn, a successful prosecution.

Solving A Money Laundering Investigation In Record Time

A complex $150 million healthcare fraud scheme involving a pharmacist and fraudulent claims to federal healthcare programs left government investigators overwhelmed by the sheer volume and complexity of the data.

Traditional manual methods were proving time-consuming, leaving a backlog of cases and hindering efforts to stop the misuse of taxpayers’ money. The scheme, involving unnecessary compounded medications for patients, required a precise and sophisticated solution.

ScanWriter’s advanced data entry automation and automated data visualization of the flow of funds assisted investigators in quickly uncovering the case. The tool reduced data input time from months to weeks and provided a more accurate and efficient solution than previous methods.

The Future of Asset Misappropriation Investigations

Asset misappropriation investigations are facing new trends and challenges that require both awareness and adaptation by federal fraud investigators.

The globalization of fraud schemes, fueled by an interconnected economy, adds complexity to investigations and requires cross-jurisdictional cooperation. Simultaneously, the rise of cyber fraud, the adoption of cryptocurrencies, continuous regulatory changes, and increasingly sophisticated insider threats are posing new challenges.

Given these emerging challenges, leveraging technology becomes an essential part of modern fraud investigations.

- Data Analytics and Automation: Tools like ScanWriter can reduce the manual labor involved in data entry and analysis, cutting down the time it takes to process vast amounts of information.

- Machine Learning and AI: Implementing AI algorithms and machine learning can help in identifying patterns, anomalies, and predictive indicators of fraud, providing insights that might be missed by human analysis alone.

- Digital Forensics: As fraud becomes more digital, investigators need specialized tools to analyze electronic evidence, trace cyber footprints, and uncover hidden information within digital devices.

Wrapping Up

The fight against asset misappropriation fraud is an ever-evolving battle, with federal fraud investigators at the forefront.

In this challenging environment, tools like ScanWriter can provide you with incredible assistance, transforming the way investigators handle massive data, detect patterns, and streamline processes to protect the integrity of financial systems.

Request a demo for ScanWriter today!