In February of 2021, a Ukrainian man was sentenced to 87 months in prison and to pay restitution of $98,000 for wire fraud, stemming from his participation in a scheme to launder funds for Eastern European cybercriminals.

From 2009 to 2012, Aleksandr Musienko’s partners hacked into online accounts of U.S. companies and stole funds which were then transmitted to accounts overseas.

Musienko was involved in recruiting, supervising and directing a network of “money mules” who, hired as “financial assistants,” believed they were helping clients transfer funds overseas.

In Sept 2011, Musienko’s partners hacked into the online accounts of a North Carolina-based company and transferred a total of $296,278 to two bank accounts controlled by Musienko’s mules.

The rise of digital financial services has opened the door to criminals who leverage the internet and other digital platforms for criminal activity and to conceal and move illegally obtained funds.

Whether it’s cyber laundering or money laundering, the hiding and reinvestment of illegal profit made from a criminal enterprise is key to creating distance from criminal acts and the key to running a successful crime organization.

And it’s also a critical juncture for detecting and disrupting criminal activity.

Following the Money Mule Trails

In order to create distance from their criminal activities and profits, criminals need to “employ” people who are “innocent” and have no ties to the original crime.

For this reason, money mules are the first step in the wash cycle.

In the past, money mules were known to cross borders with money strapped to their bodies or travel with briefcases or car trunks full of cash.

These days money mules can work from home, using online banking to transfer money through bank accounts, digital currency, prepaid debit cards, or money service providers.

Electronic laundering cleans illegally obtained funds of their dirty criminal origins for use within the legal economy.

Money mules are recruited through job ads promising easy money for little or no effort.

Money mules, usually students, people out of work, or the lovelorn, are typically asked to open new bank accounts in their name or company. They’re then asked to use these accounts to receive and transfer funds via ACH, mail, or wire transfer. For their efforts, they’re often given a commission or flat fee.

In this way, transnational criminal organizations use mules to channel funds across institutions or borders to obscure the source of funds.

Money mules are also roped in through dating or social media sites and asked to receive money and then forward these funds to one or more individuals they don’t know. Believing they’re helping a loved one in need, these money mules unwittingly break the law and aid one more criminal enterprise to disguise their ill-gotten gains.

Though some money mules are unwitting accomplices, others know they’re supporting criminal enterprises and do it out of desperation, sloth or greed.

Either way, money mules can be prosecuted and incarcerated for their part in this illegal activity that helps criminals cash out of fraudulent schemes and transform illicit funds into legal tender.

Bank Secrecy Act Helps Flag Illicit Transactions

In order to deter money mules and their “employers,” the Bank Secrecy Act (BSA) was created in 1970 to prevent financial institutions from being used by criminals to hide or launder their illicit earnings.

The law prescribes regulations and procedures banks or other financial institutions must follow to detect and deter money laundering.

If a bank uncovers suspicious activity that might be related to money laundering, they’re required by law to file a Suspicious Activity Report (SAR) with the Financial Crimes Enforcement Network (FinCEN).

As part of a SAR and to justify the report, a bank must include all available data related to the suspicious activity.

An investigation like this takes time. Analyzing mountains of data and hundreds to thousands of pages and reports can slow down a process that must be done quickly. Banks have 30 calendar days after the initial detection of the incident to file a SAR.

Traditionally, investigators have had to do a great deal of manual work sorting through the vast data required by the BSA. These methods are time-consuming and may be inefficient, leading to a higher number of backlogged cases.

Investigative tools must keep up with ever-changing technologies in payments and transactions. And automation is emerging as a powerful solution.

Also read: Your A To Z Guide To Preparing a Compelling Narrative For Suspicious Activity Report.

ScanWriter Automation Speeds Investigations

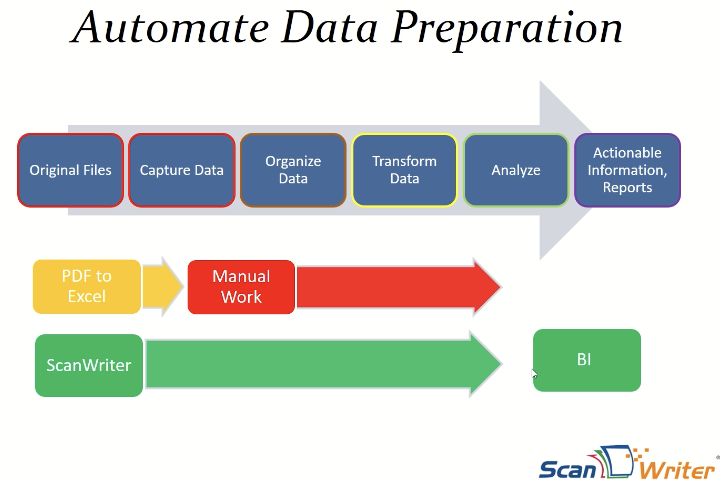

ScanWriter, developed by Personable, is rapidly becoming an essential asset for data preparation and visualization in financial investigations. By automating data entry and generating reports, ScanWriter allows investigators to sort and analyze data quickly, providing insights that can lead to the discovery of fraud, money laundering, and other illegal activities.

Collaboration and organization are critical to successful outcomes in fraud cases, and ScanWriter provides a single platform for safe and efficient collaboration. It allows users to collect and organize data from various sources and share information across departments, streamlining investigations and facilitating prosecutions.

With its easy-to-use interface and data visualization capabilities, ScanWriter is ideal for financial fraud investigators looking to trace hidden assets. Its data entry automation feature converts paper documents and digital files into normalized data on Excel, processing large files in minutes with precision.

ScanWriter sorts and categorizes transactions by type or customizable categories, streamlining case workflows and generating organized Excel spreadsheets. Data visualization capabilities include pre-created models such as the “Flow of Funds” model, which illustrates the movement of money in a visually immersive and interactive way.

Customizable to any case strategy, ScanWriter’s data enrichment displays captured data in a format that shows the connections between data points, making patterns and insights easy to understand at a glance. Overall, ScanWriter saves investigators precious time and resources during data preparation, creating data visualizations that provide insights for successful outcomes.

Also read: Asset Tracing: How Technology Can Help Fraud Investigators Follow The Money To Trace Assets?

In Summary

ScanWriter is the perfect tool for every step of an internal SAR investigation, with its ability to sort and analyze critical transactions quickly and accurately. This on-premise solution is ideal for high-security environments, processing and saving files locally, and comes with a dedicated tech staff to provide support when needed.

Designed for today’s online financial investigations, ScanWriter detects and analyzes inconsistencies, trends, and patterns, making it an efficient and reliable solution for detecting and preventing fraud.

Trusted by district attorneys, forensic accountants, and fraud investigators across the USA, ScanWriter boosts productivity by 90% with its time-saving features, benefiting businesses of all types.

With its ability to speed up the data sorting process and uncover the trail of criminals and money mules and their illegal activities, ScanWriter saves investigators valuable time and resources.

No matter the challenges your organization faces, ScanWriter offers an effective solution. Contact us today for a free demo and experience the power of ScanWriter’s data automation solutions to save time and money.