Currently identified as the most rapidly expanding financial crime in the U.S., Synthetic Identity Fraud is on track to cause staggering losses estimated at US$23 billion by 2030. This trend doesn’t show any signs of diminishing.

But what’s fueling its growth?

From the perspective of a fraudster, the appeal is clear: creating synthetic identities is not only cost-effective but also carries a significantly lower risk of detection. The recent advancements in artificial intelligence, which can now closely mimic real identities, combined with the easy access to personal data (known as Personally Identifiable Information or PII) on the dark web for as low as $15, have made it increasingly simpler for fraudsters to perpetrate these crimes.

As said by R. Sean McCleskey, a retired United States Secret Service agent, in his interview with CNBC, “When criminals use a blend of different people’s data, as well as some entirely made-up information, it becomes harder for law-enforcement officials to both realize the crime and then locate the culprit.”

To help investigators decode this sophisticated fraud scheme, our article goes over all the elements that make up the infamous synthetic identity fraud along with actionable solutions to investigate the synthetic identity fraud you can start implementing right now.

But First, Let’s Understand What is a Synthetic ID

A synthetic ID is a fraudulent identity that combines stolen information from real people with fake details to create a new one.

For instance, imagine a carefully crafted persona composed of a stolen Social Security number, a fabricated name and address, and a mix of believable details. This, in essence, is a synthetic identity.

Fraudsters wield these identities to open bank accounts, obtain loans, and make lavish purchases, leaving real people and financial institutions with critical consequences.

Here’s a Real Life Example of Synthetic Identity Fraud

In a high-profile case, a California couple executed a sophisticated synthetic identity fraud scheme to fraudulently obtain over $20 million in COVID-19 relief funds. Convicted by a federal jury, the duo fled the United States after sentencing and spent over a year as fugitives in Montenegro.

The couple, part of a Los Angeles-based fraud ring, utilized dozens of fake, stolen, or synthetic identities, including those of elderly or deceased individuals and foreign exchange students.

They submitted approximately 150 fraudulent applications for Paycheck Protection Program (PPP) and Economic Injury Disaster Loan (EIDL) funds, supporting these applications with false documents, such as fake identity papers, tax documents, and payroll records.

What makes this case notable is the extensive use of synthetic identities to deceive lenders and the Small Business Administration. The fraudsters exploited traditional banking processes and acquired luxury assets, including three homes, gold coins, diamonds, jewelry, watches, furnishings, designer items, and a Harley-Davidson motorcycle, further complicating the financial trail.

Must read about the 6 leading types of identity frauds in U.S. in 2023!

How Can Synthetic Identity be Created?

Fraudsters compile a mix of genuine details and fabricated information, including names, addresses, and other personal identifiers. These elements are carefully curated from various sources to ensure the Synthetic Identity aligns seamlessly with existing data patterns.

Depending on the methods fraudsters use to forge these deceptive identities, Synthetic IDs can be broadly classified into the following two types:

Manipulated Synthetics

In this approach, fraudsters take a real identity and tweak it subtly. A slight change in the SSN, a birthdate shift, or a new address – these seemingly minor alterations can be enough to fool verification systems and establish a fraudulent persona.

Manufactured Synthetics

These IDs, also referred to as ‘Frankenstein identities,’ are built together from stolen data, often collected from data breaches or the dark web. This information is mixed with fictitious elements to create a new fraudulent identity.

For instance, a fraudster may combine a legitimate SSN from one individual, residential details from another, and a fake employment history, resulting in a ‘Frankenstein’ identity.

More recently, an additional issue is contributing to the rise of synthetic identity fraud. Social Security numbers (SSNs) are now randomized rather than based on geographic location, which has made it more difficult for companies to identify anomalies indicative of these types of fraud.

Must Read: Four anti-fraud trends to watch for in 2024

Why is Detecting or Investigating Synthetic Identity Fraud Such a Big Challenge?

In contrast to completely fake IDs, synthetic identities use genuine elements from a real person’s documents. This way, fraudsters can bypass various identity checks, including the KYC, making it more difficult for investigators to detect irregularities, especially when fraudulent activities span months or even years.

Here are some of the top reasons that make it challenging to detect Synthetic Identity Fraud.

#1 Volume of Transactions

Fraudsters build creditworthiness and legitimacy over extended periods before committing the fraud, often called the “bust-out fraud.” This sustained activity allows them to operate under the radar, avoiding immediate suspicion.

As time increases, the sheer volume of data makes identifying suspicious patterns incredibly difficult. When the criminals finally use these accounts for fraud, financial institutions may only take action after multiple missed credit card payments or the occurrence of suspicious chargebacks. Unfortunately, criminals have often siphoned off substantial amounts when the account is flagged for closure.

#2 High-Value Investments

Synthetic identity fraud is often used to launder money by funneling illicit funds into high-value assets, such as real estate or jewelry. These identities are designed to leave minimal digital footprints, making it difficult for investigators to trace the funds back to the perpetrators.

Traditional tracking methods are not always effective in tracing the flow of funds in these cases. Fraudsters can exploit the limitations of these methods, utilizing them as opportunities to conceal their ill-gotten gains.

#3 Organized Rings

Synthetic Identity fraud is rarely a solo act. Organized rings operate as interconnected entities, each playing a specific role in executing these fraud schemes. It often involves individuals with specialized skills, such as identity creation, financial manipulation, and evasion tactics.

This makes it imperative for fraud investigators to utilize cutting-edge investigation tools and engage with experts from diverse fields such as technology, finance, and law to understand and counteract the multifaceted strategies used by organized rings. For instance, institutions can leverage the Link Analysis technique to identify relationships between different nodes. These nodes can include people, organizations, and transactions.

#4 Global Nature of Synthetic Identity Fraud

Fraud schemes transcend geographical boundaries, making investigations inherently more complex.

Due to the global nature of synthetic identity fraud, investigators must deal with diverse regulations, share intelligence, and collaborate internationally to combat it effectively.

#5 Deepfakes and AI for Synthetic Identity Fraud

Artificial intelligence can analyze and mimic human behavior, making the generated identities more convincing and resistant to traditional detection methods.

Deepfakes leverage these AI algorithms to create highly realistic, computer-generated content, including videos, audio recordings, and images. The problem emerges when fraudsters exploit deepfake technology to generate lifelike personas that are challenging to distinguish from genuine identities.

Also Read: Top 7 Bank Statement Extraction Software for Federal Agencies

Combat Synthetic Identity Fraud with ScanWriter

To effectively investigate synthetic identity fraud, it is critical that investigators have advanced tools to detect anomalies and identify patterns within the given data at the right time.

ScanWriter stands out as a powerful partner, offering a wide range of solutions designed to tackle the complexities introduced by these modern fraud schemes.

Source: ScanWriter

Trusted by several federal and state government agencies, ScanWriter equips fraud investigators with the capabilities needed for efficient fraud detection and prevention.

Here what you’ll get:

#1 Automated Data Capture

As discussed earlier, Synthetic Identity Fraud often involves a high volume of transactions spread over extended periods.

Manually entering data to find these anomalies is time-consuming and prone to errors, which provides enough opportunities for fraudsters to hide their scams.

Fortunately, there is a solution – investigators can use ScanWriter’s automated data capture to address the volume challenge and eliminate the risk of human error. The software utilizes state-of-the-art optical character recognition (OCR) to help you with swift and automated data extraction.

Here’s how our software can help you with efficient fraud investigation:

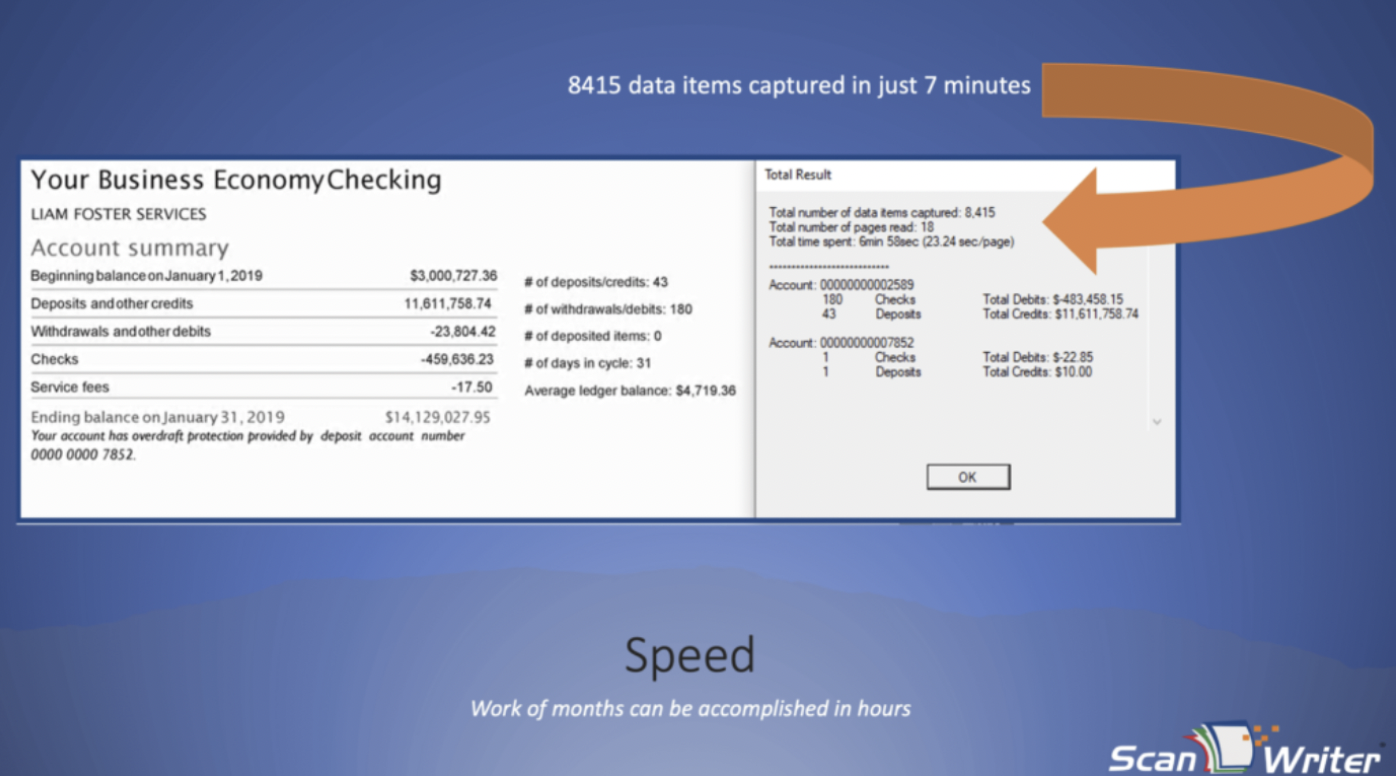

- ScanWriter supports 15000+ bank formats from financial institutions all over the world. Investigators can simply upload various financial documents, including bank statements, checks, and transaction records. Our state-of-the-art algorithms swiftly translate raw data into structured spreadsheets, freeing experts from time-consuming data entry tasks and allowing them to focus on insightful analysis.

- The software guarantees 100% accuracy for the captured data. Remarkably, it can even read handwritten checks with an additional zoom-in feature to decipher difficult handwriting.

- Investigators can process hundreds of documents simultaneously by leveraging ScanWriter’s batch processing feature. For instance, the software can read 1,000+ checks in less than an hour with 100% accuracy.

Investigators can also set specific rules in ScanWriter, allowing for data normalization and ensuring a consistent format across all entries. This streamlining of investigations results in quicker and more accurate analyses, empowering fraud investigators with a robust tool for combating synthetic identity fraud.

#2 Powerful Data Visualization

Having data isn’t enough; it needs to be refined to gain valuable insights. Powerful data visualization software can help identify connections inherent to synthetic identity fraud that may not be immediately apparent in traditional analyses.

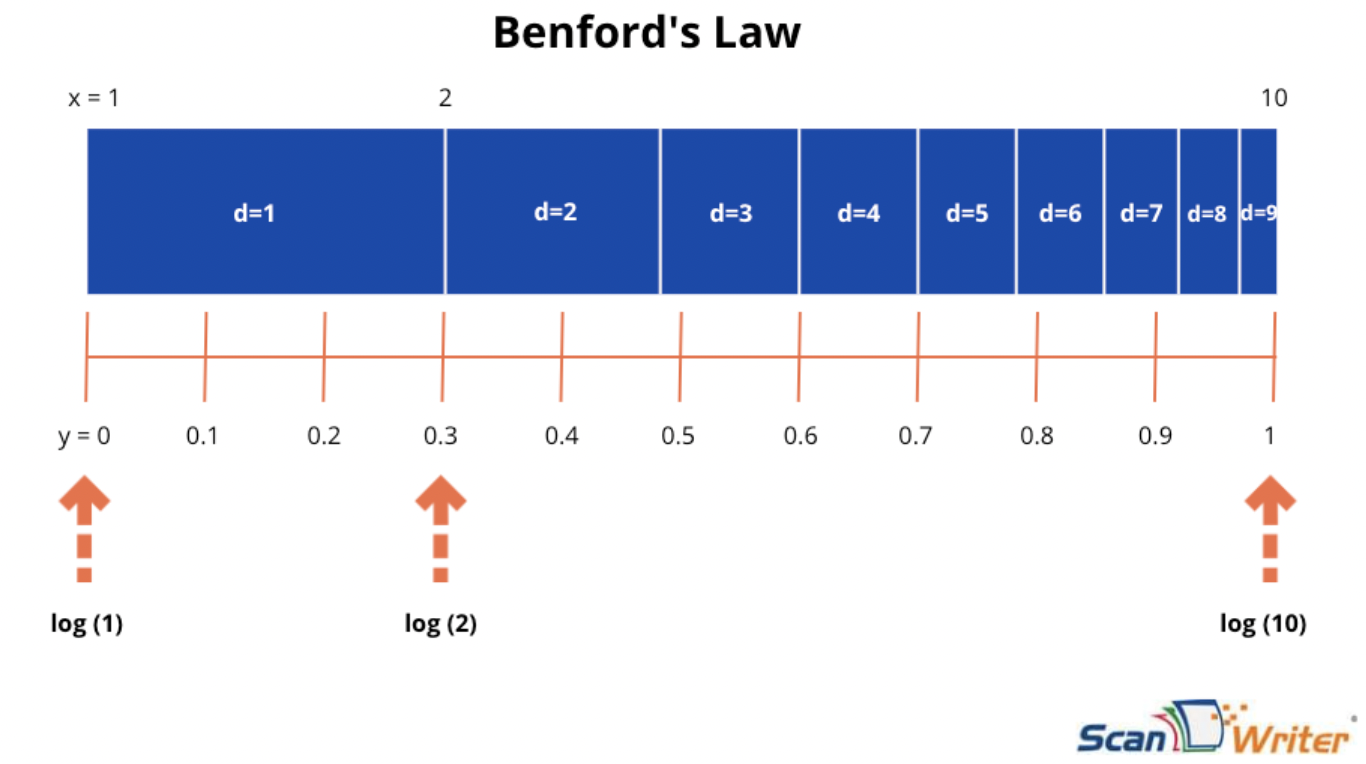

ScanWriter’s advanced data visualization feature, developed in collaboration with Microsoft Power B.I., can autonomously turn your data into coherent, visually immersive, and interactive insights. To help investigators further, the software comes with a library of predefined models to choose from, including “Flow of Funds,” “Benford’s Law,” and “SAR Analysis”.

For example, ScanWriter can provide you with visualized data using Benford’s rule without requiring manual calculations. It compares the expected distribution of the first digits to the actual distribution of the first digits. Any first digits significantly more or less common than expected are flagged as suspicious.

#3 Asset Tracing

Understanding the flow of illicit funds is critical in combating synthetic identity fraud. ScanWriter’s asset tracing capability tracks financial transactions and helps uncover connections between different entities.

For instance, investigators typically manually create financial models in Excel, which can be tedious. ScanWriter not only automates the population of these financial models with accurate data captured, but it also provides additional functionality to help investigators discover hidden assets. For example, investigators can filter data visualizations to follow the money trail for a particular person or entity.

Investigators can then precisely follow the money trail, gaining insights into suspicious transfers, luxury purchases, and connections associated with synthetic identity fraud

#4 Cross-Border Analysis

As synthetic identity fraud knows no geographical boundaries, investigators often need to conduct cross-border analyses. With ScanWriter’s powerful data capture and visualization capabilities, financial investigators can not only trace the money trail globally but also uncover crucial evidence quickly.

ScanWriter also provides investigators with a layered audit trail using forensic accounting tools. The audit trail is embedded in Excel files, making it easy for investigators to find associated PDFs.

On top of that, with the support of 21 languages and access to the libraries of more than 40,000 institutions, including more than 10,000 financial institutions, ScanWriter can help detect synthetic identity frauds with precision and time efficiency.

If the document format you need is not already present, you can also request a new document format and we can add it within 24 to 48 hours of your request.

Here’s a Real Life Case Study

A married couple engaged in money laundering through a fictitious restaurant, employing a scheme to conceal their illicit gains.

The business’s bank statements highlight numerous deposits from a small group of purported customers, each making unusually large, round-numbered deposits, such as $10,000 per customer.

Recognizing this suspicious pattern, ScanWriter promptly raised red flags. Upon closer investigation, it was revealed that the restaurant, as claimed, did not exist.

The listed business address turned out to be a vacant building that was up for sale. Compounding the deception, the restaurant had dubious transactions with a currency exchange business in Mexico. Dollars were funneled to Mexico, where they were converted into pesos. Subsequently, the acquired pesos were used to procure high-value assets like condominiums, airplanes, and other luxury items.

ScanWriter’s robust data visualization tools, including ‘flow of funds’ and ‘follow the money’ financial models, were pivotal in tracing these assets.

A Quick Wrap-Up

Confronting synthetic identity fraud requires a modern approach, as traditional security measures often fall short. These cunning fraudsters expertly exploit system vulnerabilities, completing their schemes before the flaws are even noticed.

To stay ahead of these intricate frauds, investigators and financial institutions must embrace cutting-edge solutions. This is where ScanWriter, a robust investigation tool, enters the fray.

Seamlessly integrating popular platforms like Excel, QuickBooks, and Microsoft Power BI into the software, ScanWriter offers an immediate boost in investigations, ensuring no anomalies go unnoticed. Its installation is straightforward, enabling swift utilization. Plus, our dedicated support team stands ready to assist you in mastering your initial data captures.

Discover the full potential of ScanWriter and how it can revolutionize your fraud investigation strategies. Take the first step and request a free demo to experience our premium features firsthand.

FAQs

#1 What are the warning signs of synthetic identity fraud?

There can be multiple signs that a fraudster may be using a synthetic identity to carry out their activities including:

- Inconsistencies in personal information

- Unusual spending patterns and discrepancies in credit reports.

- Frequent changes to account details

- Multiple accounts linked to a single identity

- Unusually high transaction volumes for a given profile.

Vigilance in monitoring these indicators is crucial for early detection and prevention of synthetic identity fraud.

#2 What preventive measures can individuals and organizations take against synthetic identity fraud?

Preventing synthetic identity fraud requires a multi-faceted approach:

- Enhanced Verification: Implement robust identity verification processes, incorporating biometrics and advanced technologies.

- Monitoring and Analytics: Regularly monitor for unusual patterns in financial transactions and apply advanced analytics to detect anomalies.

- Education: Educating individuals and employees about the risks of sharing personal information online and encouraging vigilant monitoring of their financial accounts is important.

- Collaboration: A good idea is to promote collaboration between institutions and regulatory bodies to share information on emerging threats and best practices.

#3 What role does ScanWriter play in fraud investigation?

ScanWriter provides investigators with advanced tools for combating fraud. For instance, the software swiftly and accurately extracts data using OCR technology, while the asset tracing feature enables investigators to follow the money trail meticulously. In collaboration with Microsoft Power B.I., ScanWriter delivers powerful data visualization, aiding investigators in discerning intricate connections between entities across the globe.

#4 Can ScanWriter read financial documents from a credit union?

Yes, ScanWriter can accurately capture data from financial documents of a credit union. Additionally, ScanWriter allows for the addition of new document formats within 24 to 48 hours of request. This adaptability ensures that investigators can decode any documents to combat emerging synthetic identity fraud schemes, staying one step ahead of fraudsters.

#5 Can ScanWriter be customized to specific investigative needs?

Absolutely. ScanWriter offers customization options to tailor the software to specific investigative requirements. Whether it’s adjusting data normalization rules or creating specialized data visualization models, investigators can customize ScanWriter features to address the unique challenge during synthetic identity fraud investigations.